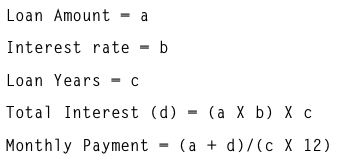

Rule of 78

According to LoanStreet – The Rule of 78 is one of the most prevalent secrets in the banking industry that

Capturing Moments, Unleashing Emotions: Photography Beyond the Lens.

Capturing Moments, Unleashing Emotions: Photography Beyond the Lens.

According to LoanStreet – The Rule of 78 is one of the most prevalent secrets in the banking industry that

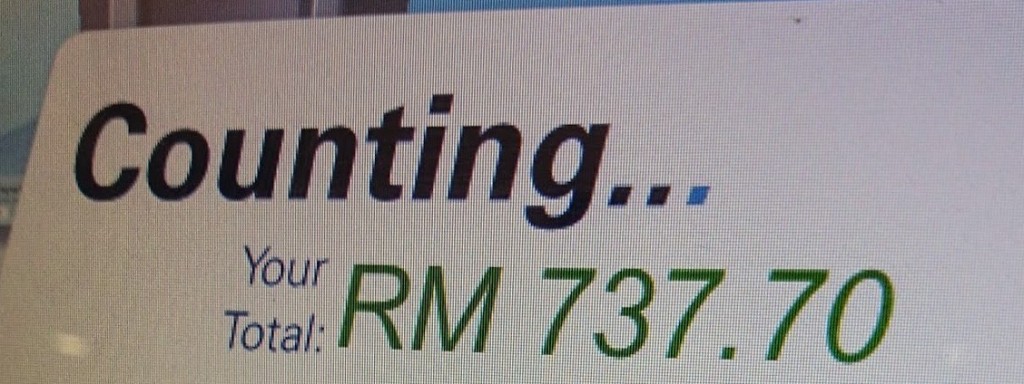

In the past year, I’ve been losing my memory! Or rather been a bit too careless. There have been many

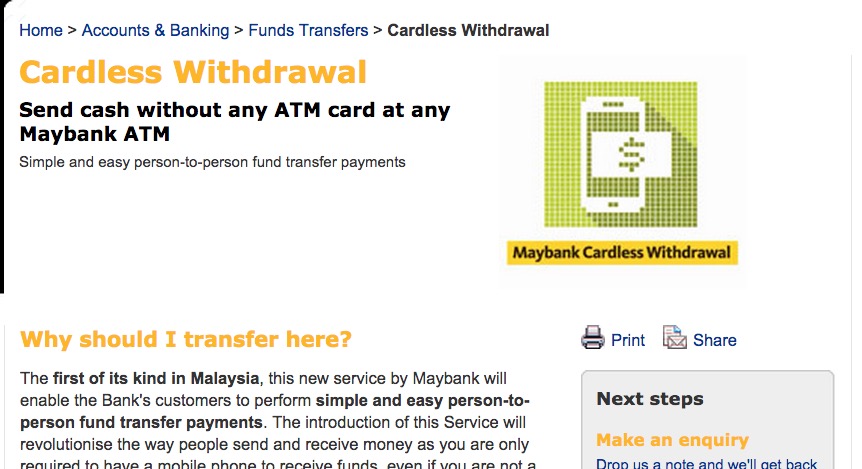

Generally in my daily life, I really hate carrying coins. In fact, most of the occasions I would leave the