Risk Management Functions

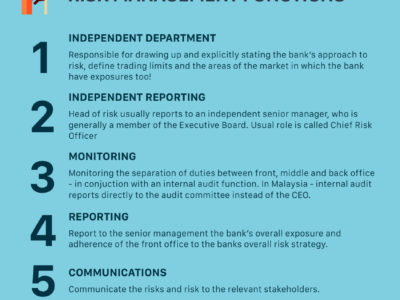

Another one of my learning infographics. As a continuation from the previous posting on Bank Risks – this is the risk

Capturing Moments, Unleashing Emotions: Photography Beyond the Lens.

Capturing Moments, Unleashing Emotions: Photography Beyond the Lens.

Another one of my learning infographics. As a continuation from the previous posting on Bank Risks – this is the risk

As part of my learning journey in banking – suddenly today I felt like doing some infographics of what I

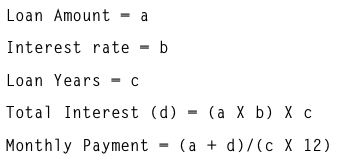

According to LoanStreet – The Rule of 78 is one of the most prevalent secrets in the banking industry that