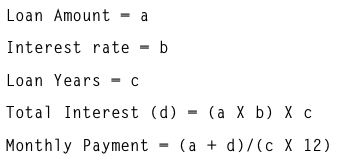

Rule of 78

According to LoanStreet – The Rule of 78 is one of the most prevalent secrets in the banking industry that

Capturing Moments, Unleashing Emotions: Photography Beyond the Lens.

Capturing Moments, Unleashing Emotions: Photography Beyond the Lens.

According to LoanStreet – The Rule of 78 is one of the most prevalent secrets in the banking industry that

I have been a resident of my current place for more than 14 years. Probably bordering 15 years. Honestly this