EPF is a great retirement platform for working individuals to strive towards a comfortable retirement.

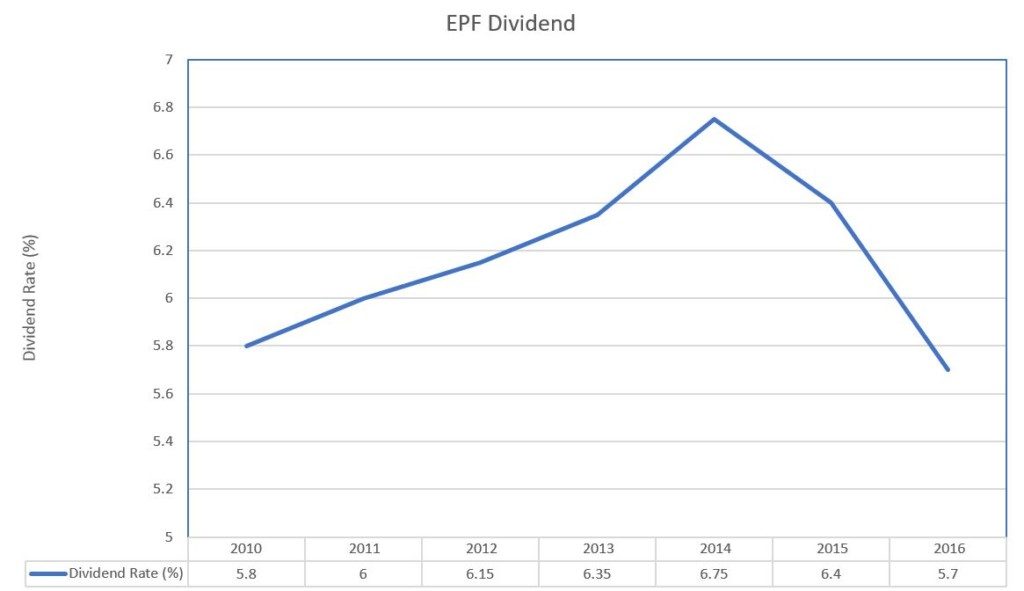

That’s the hypothesis that I have. Consistently EPF has given me a good return of investment. Or at least in the past couple of years. Look at the chart below on the dividends that are issued by EPF.

In 2016, we get 5.7%. That’s pretty awesome. Even fixed deposit won’t be able to get us that returns. A closer fund would be Amanah Saham Bumiputera or in short ASB. In he past ASB has given us returns in the region of 7-10%. In fact there were days in which we gotten more.

Anyway – EPF is a forced saving. No matter what you do if you are employed, we are obliged or required to put in our EPF.

Part of my retirement strategy is to rely on EPF as a source of funds. I do hope that the returns from EPF doesn’t go bonkers in the next 6 years!

In fact – I am also looking at other options to distribute the risks but nevertheless it is important to have that capital baseline that will help you to generate the funds required to help support you. Yes it is a lot of work and discipline but that if we don’t have a plan now, we would not know when we would be able to reach where we want to reach or achieve.

The key to all this is of course discipline and hard work. I have 6 years to go and I still have a lot more work to do. I can’t afford to take big risks therefore focus on getting what I want. It might be hard but we need to do what we need to do. Focus focus focus focus.

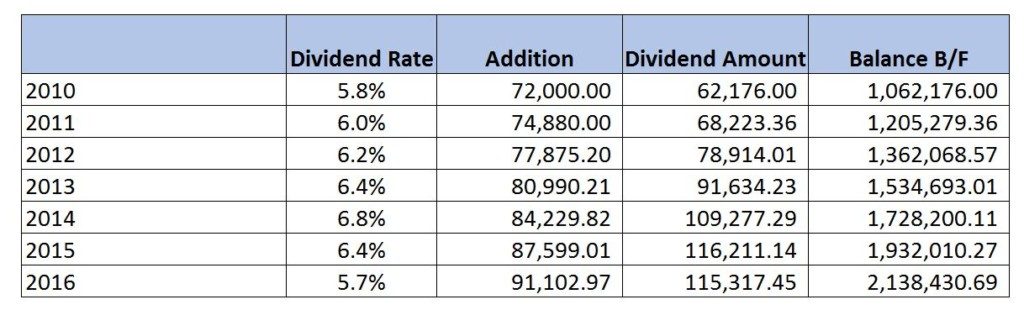

So back to the EPF… here is a table of returns if:

- we have a capital baseline of 1M

- contribution of 6k per month at year 1 (inclusive both employer and employee).

- increase of contribution of 4% on year on year basis

You can see if you do have a good capital baseline, in a very short period(7 years) we would be able to make quite sizable money at the end of each calendar year from the dividend!

Note that after 1.05M, we can withdraw money from EPF. So it’s extremely important to get a baseline of that amount in order to be able to remain liquid when you retire.

The problem is of course the following:

- You will need a good capital baseline to start. To get 1M in EPF not going to be so simple!

- You will also need to earn at least 30k in order to get 6k contribution.

Question? 100k a year without debt. Can you retire? That translates to approximately about MYR8333 a month. If you are without debt, it is actually not a bad amount. How much money can you spend anyway. If you spend a lot of time spending of course you are screwed. But for me if i reach this level, I would probably just take MYR4000 to spend and the rest of it I will leave it for my savings. At the end of the day – MYR4000 is a lot of money to spend. This translates to MYR133 per day to spend! If i cook myself I probably only need about MYR10-20 to have few good meals.

If one would need to travel, one will probably need another travel bucket that we need to create to support what you want to do. Yes MYR8000 a month for travelling is enough but the problem is if we spend all the money for travelling, we are not helping to replenish the capital baseline. Which may deplete due to the inflationary rates which is probably in the region of 3% in Malaysia!

**numbers above does not reflect what i have, probably a far cry… :(**