According to LoanStreet – The Rule of 78 is one of the most prevalent secrets in the banking industry that is barely understood by the public. This post is about me trying to understand how it works, and hoping to share with you so that you understand and be able to figure out how you can apply it to your financial decision.

Since I got to banking I am in a learning mode. Learning how the banking system work. Being a self-professed technical person, I will try to understand things in a more technical way. Whether for good or bad.

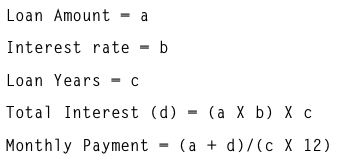

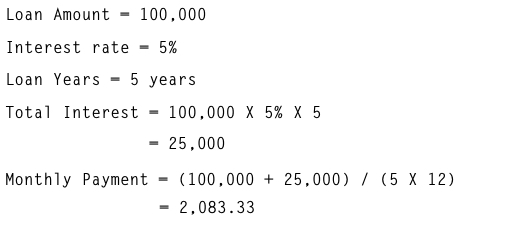

The situation now is that I am buying a new car and deciding how many years should I take up the loan. And since I am not yet eligible for staff loan yet, I need to resort to a conventional loan from other local banks that offer Hire Purchase. So in order to calculate this – I need to understand how the settlement works. Well – fact of the matter the settlement is done by returning back to you the interest that was charge. Do understand that for typical hire purchase here is the formula:

So what this mean is that the interest are charge up front when you take the loan,

Question is now, when you terminate your loan, how do you calculate the interest that will be returned? Well – generally its calculated by “Rule of 78”. What this rule essentially says, the borrower will be paying greater part of the interest during the initial part of the loan. I.e, more interest are apportion during the first year versus in the later years. Note that this is different from the “Daily Rest” or “Monthly Rest” types loan in which the interest are always calculated based on the outstanding balance prorated to the period.

Example “Daily Rest”, the interest rate is divided by 365 days and then applied daily based on the outstanding amount that the borrower has. This should be better because as one pay earlier, the outstanding amount will be less and therefore the knocking off the principal amount is faster. Note that when you pay, interest will be the first to be paid before the principal. Principal is the original loan amount. So if one is smart, you will be able to “game the system” and able to pay less interest if you know when to pay your loan.

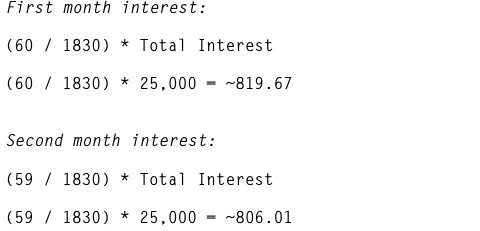

Back to Rule of 78. So the question is how do you calculate the weightage? Lets take an example above, 5 years loan. A lender would make a sum of all the months:

![]()

So basically what happened is this, the way the interest is calculated is in reverse. I.e. interest for the first month is based on the assumptions above:

Which make it quite interesting because if the weightage of the interest is fair, then the total interest that will be refunded will be a lot less if you were to settle earlier.

So what I did in order to calculate how long is my loan duration is for me to plot a table of the settlement price versus the depreciation of the car and eye ball for a sweet point in which I am willing to sell off the car. I will explain that in another post. But I hope you do get what I mean by Rule of 78.

You may think that this may not seem fair for the borrower, but you need to understand that for a bank, each of the loan has a lot of cost thats associated to it. From creating the infrastructure to manage the balances to hiring sales people to push the loans. And thus they need to be able to make money out of the lending that they do to their customers.

I hope the post is somewhat beneficial. Remember please do read the terms and conditions of your hire purchase or loans and see if Rule of 78 applies. They may not say specifically that they use Rule of 78, but you can see that the calculation is similar.

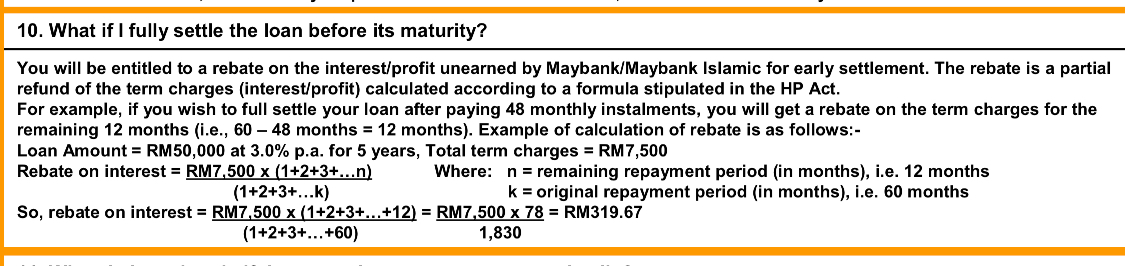

Taken from here Maybank. Link may not work… 🙂

Note; I am not a financial advisor therefore I am not responsible for any inaccuracy of the information posted here. Please do your own research and consult professionals if you need any advice regarding your financials. I wrote this post to poke my readers curious minds 🙂